The conference room inside a glass tower in Marunouchi felt like a theater of polite resistance. A team of elite cross-border M&A advisors from New York sat across from the independent directors of a historic Japanese retail conglomerate. The Western team presented a fully financed, premium-valued tender offer that promised an immediate forty-percent upside to the public shareholders. They displayed beautifully rendered spreadsheets detailing capital efficiency, synergy metrics, and immediate cash returns.

The response from the Japanese side was a masterclass in elegant immobility. The chairman bowed slightly, smiled warmly, and stated that a newly formed special committee would evaluate the proposal with absolute diligence.

Months passed in complete silence. The digital data room remained a desert of public filings. Scheduled management meetings were repeatedly rescheduled due to sudden scheduling conflicts. High-ranking domestic executives quietly failed to attend crucial coordination calls, sending junior representatives with no decision-making authority in their place.

The foreign suitor eventually realized that their multi-billion-dollar valuation was completely irrelevant to the current leadership. The board was deploying the classic defensive architecture of the Tokyo establishment: a calculated strategy of systemic delay, administrative friction, and deliberate pace-management designed to exhaust the outsider’s patience and capital reserves.

The Architecture of Interlocking Capital

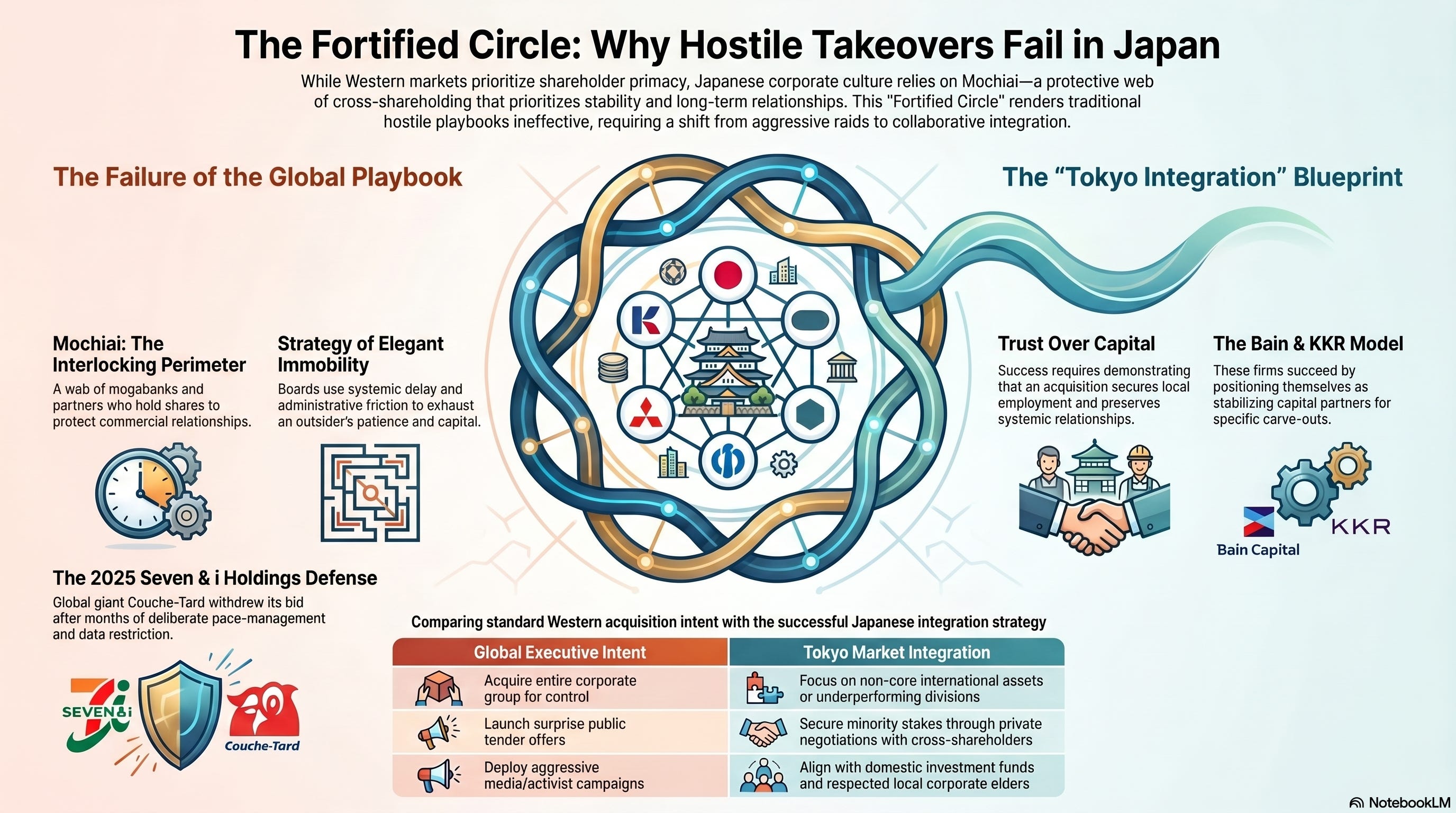

This systemic resistance to external corporate raids reflects the enduring legacy of Mochiai, the historical practice of cross-shareholding. While Western capital markets operate on the principle of shareholder primacy, where the highest bidder routinely wins control of an asset, the Japanese corporate ecosystem prioritizes stakeholder stability and community preservation. In this model, a company’s shares are held securely by a protective web of domestic megabanks, life insurance firms, and long-term supply-chain partners.

These friendly shareholders form an invisible perimeter around incumbent management. They view their equity stakes as a mutual insurance policy to protect commercial relationships rather than a liquid financial asset to be traded for a short-term profit. Their primary allegiance belongs to the longevity of the enterprise and the maintenance of market harmony. Consequently, when an unsolicited bidder launches a hostile tender offer, the target firm can rely on this network of institutional allies to support the current executive board, effectively neutralizing the leverage of public market arbitrage.

The historic corporate battle of 2025 perfectly illustrated the durability of this protective framework. The Canadian retail giant Alimentation Couche-Tard launched a massive, multi-billion-dollar bid to acquire Seven & i Holdings, the parent company of the global 7-Eleven empire. The offer represented one of the largest foreign takeover attempts in Japanese history, occurring at a moment when the Tokyo Stock Exchange was actively pushing for greater capital efficiency and enhanced shareholder rights.

Despite intense global scrutiny and regulatory pressure, the traditional defense mechanism held firm. Seven & i Holdings established a special committee that successfully engaged in a multi-month campaign of deliberate pace-management. They restricted access to material operational data and channeled the narrative exclusively into regulatory bottlenecks regarding national security and antitrust clearances.

By July 2025, Couche-Tard officially withdrew its proposal, citing a profound lack of constructive engagement from the Japanese leadership. The outcome sent a clear signal to global investment funds: even under the modern guise of corporate governance reform, a Japanese titan possesses the structural tools and the cultural mandate to stonewall an unsolicited foreign buyer indefinitely.

The Shift to Incremental Alignment

Succeeding in the Japanese corporate landscape requires a total abandonment of the hostile acquisition playbook. Brute-force capital and public proxy battles trigger defensive corporate antibodies that unite the domestic business community against the intruder. Global executives must shift their mindset toward a strategy of collaborative integration, local alliance building, and structural patience.

Influence in Tokyo is built through the steady accumulation of social capital long before the financial transaction occurs. Foreign investors must align their strategic goals with the survival metrics of the domestic firm. This means demonstrating that an acquisition will enhance the target company’s global reach, secure local employment, and preserve its systemic relationships with suppliers and creditors.

To build an authentic bridge into these fortified entities, international strategists should execute specific, affirmative operational phases designed for the local market:

1. The Carve-Out Strategy

Global Executive Intent: Acquire the entire corporate group to achieve total operational control and maximize immediate restructuring efficiency.

Tokyo Market Integration: Focus exclusively on non-core international assets or underperforming cross-border divisions. Legacy firms are highly receptive to selling offshore subsidiaries to free up domestic capital, allowing the foreign buyer to secure the desired assets while preserving the integrity and independence of the domestic parent company.

2. The Anchor Investor Blueprint

Global Executive Intent: Launch a surprise tender offer on the public stock exchange to force an immediate board vote and panic the management.

Tokyo Market Integration: Secure a minority stake through friendly, private negotiations with institutional cross-shareholders. By purchasing shares directly from domestic megabanks or insurers who are slowly unwinding their portfolios due to regulatory updates, the foreign entity enters the registry as an approved, stable stakeholder.

3. The Local Proxy Alliance

Global Executive Intent: Deploy Western activist tactics and aggressive media campaigns to publicly shame the board into a sale.

Tokyo Market Integration: Align with domestic investment funds and respected Japanese corporate elders. When a restructuring proposal is presented by a credible local ally who speaks the language of corporate longevity, the board interprets the intervention as structural stewardship that aligns with long-term survival.

Global private equity titans like Bain Capital and KKR have achieved significant success in Japan by strictly adhering to this philosophy of friendly alignment. When Bain Capital orchestrated the acquisition of Toshiba’s memory chip division, or when KKR structured the buyout of Hitachi Metals, they positioned themselves as capital partners dedicated to carving out and scaling specific business units. They worked closely with the existing management, honored corporate traditions, and maintained local employment structures. These transactions succeeded because the foreign firms operated as stabilizing forces during periods of corporate restructuring.

The ongoing updates to the Corporate Governance Code by the Financial Services Agency are accelerating the unwinding of cross-shareholdings, with major domestic financial institutions planning to continue selling these strategic stakes through 2030. This structural evolution creates a massive pool of floating capital and available equity. However, Japanese firms are utilizing this cash to fund record-breaking share buybacks and increased dividend payouts, reinforcing their independence from external control. The fortress is changing its financial architecture, yet it remains a fortress. The ultimate arbiter of a transaction is the depth of trust established within the executive suite over years of consistent, respectful engagement.

The Bottom Line

Hostile takeovers fail in Japan because corporate governance remains a system of social contracts rather than purely financial mechanisms. True corporate control belongs to those who respect the interlocking networks of domestic stakeholders and design strategies that prioritize organizational survival. Entering the Tokyo market requires a commitment to mutual prosperity that transforms the foreign investor from an external threat into an essential partner.

Over to You

Are you designing your Japanese investment strategy around the assumption of immediate shareholder leverage, or are you preparing for the multi-year process of earning the trust of the interlocking corporate inner circle?