The founder sat in the pristine, hushed lobby of a “Mega-bank” branch in Otemachi, clutching a leather briefcase that contained three million dollars in venture capital commitments and a pristine business plan. He had graduated from a top-tier global university, worked at a prestigious consultancy, and his startup was solving a critical bottleneck in the Japanese logistics sector. He possessed every hallmark of a “high-value” client. Ten minutes later, a junior clerk in a perfectly pressed uniform returned his documents with a deep, apologetic bow. The application was denied. No reason was provided. The clerk simply noted that the “comprehensive review” had concluded that the bank could not open an account at this time.

For the foreign founder, this moment feels like a glitch in the matrix. In London, Singapore, or New York, a bank exists to facilitate the movement of capital. If you have money and a legal entity, the bank is a willing partner. In Tokyo, the bank acts as a secondary regulator, a moral and social gatekeeper. The rejection was not a comment on his creditworthiness or the viability of his technology. It was a verdict on his “traceability.” To the bank, he was a ghost in the machine: an entity with capital but no history, a lease but no roots, and a vision but no “trust proxy.”

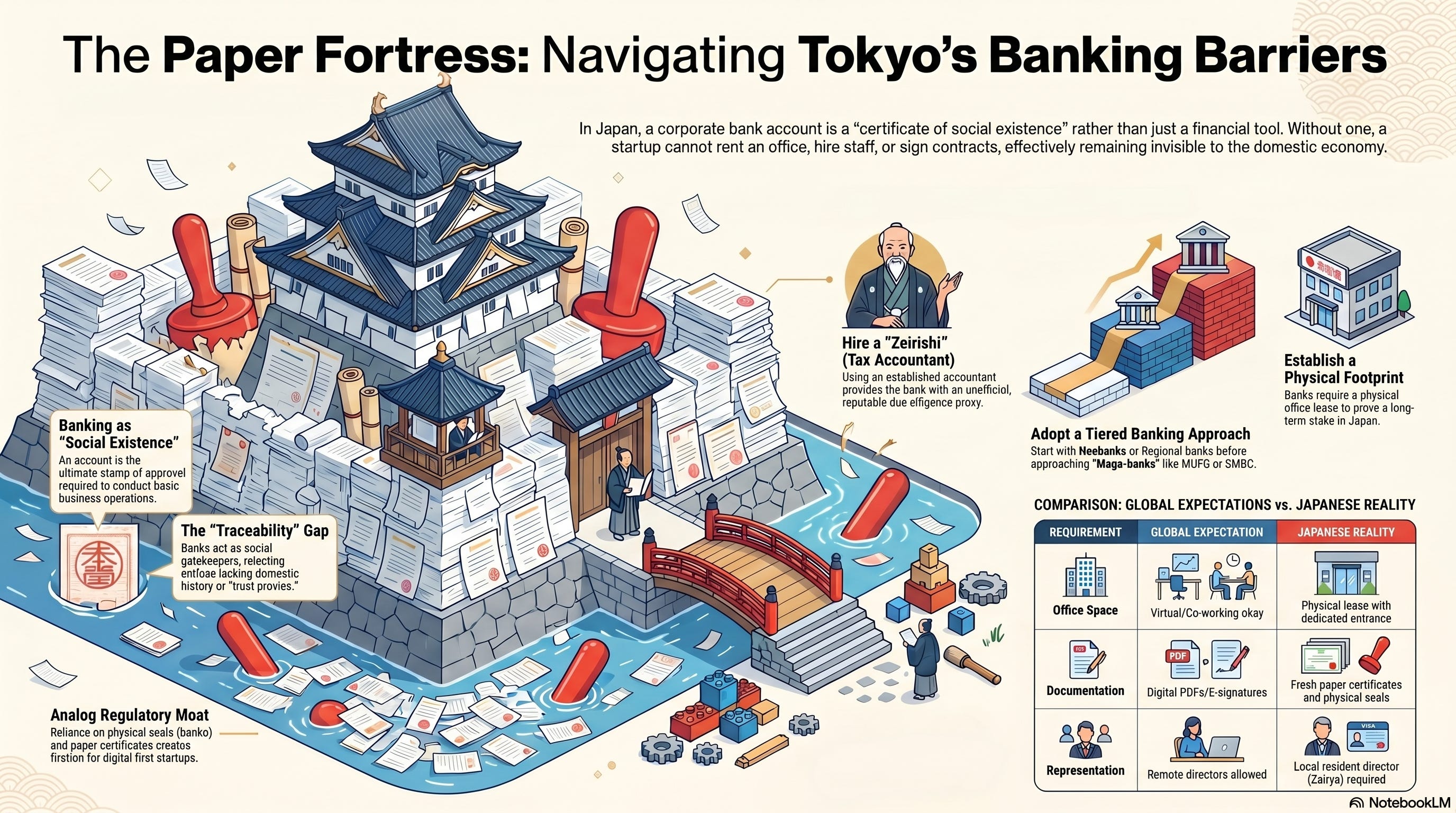

This operational wall is the single greatest hurdle for the “Global Financial City Tokyo” initiative. While the government rolls out red carpets for foreign talent, the banking sector maintains a moat of analog requirements and risk-aversion. To navigate this, one must understand that a Japanese bank account is the ultimate “stamp of approval.” Without it, you cannot rent a proper office, you cannot sign a mobile phone contract, and you cannot pay your employees. You are, quite literally, invisible to the Japanese economy.

The Bureaucracy of Existence

The resistance encountered by foreign founders is rooted in a fundamental misalignment between global startup culture and Japanese banking history. Modern startups are designed for speed, flexibility, and rapid pivots. Japanese banks are designed for stability, seniority, and the preservation of the “Main Bank” relationship. The banking sector still operates under the heavy shadow of the “lost decades,” where a surge in shell companies and financial fraud led to a culture of extreme skepticism toward any entity lacking a multi-year domestic track record.

Furthermore, Japan is under intense pressure from the Financial Action Task Force (FATF) to tighten its Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) protocols. In the Western world, banks use sophisticated AI algorithms to flag suspicious transactions. In Japan, the “algorithm” is often a manual checklist of physical attributes. If a company lacks a physical office with a dedicated landline, or if the “Representative Director” is a non-resident, the system defaults to “Reject.” The bank views the foreign founder as a “transient risk”, someone who could disappear as quickly as they arrived, leaving the bank to answer to the Financial Services Agency (FSA) for a failure in due diligence.

A definitive example of this institutional friction occurred during the recent push by the FSA to encourage “Fintech” innovation. While the central government incentivized foreign startups to enter the market, the frontline branches of the major banks (MUFG, SMBC, and Mizuho) continued to demand physical hanko (seals) and original paper certificates of incorporation (Tohyo) that were less than three months old. This “policy-reality gap” creates a situation where the right hand of the Japanese state welcomes the founder while the left hand refuses to let them deposit their investment.

Engineering the Proxy of Trust

The strategy for a successful bank application in Tokyo is a matter of “Trust Engineering.” Since the founder lacks a personal history in Japan, they must “borrow” the history of established local actors. The bank is looking for a reason to say “Yes” that provides them with an internal defense if the account ever becomes problematic. You must provide them with that defense.

The most effective “Trust Proxy” is the Zeirishi (Licensed Tax Accountant). In Japan, a Zeirishi is more than a bookkeeper; they are an unofficial arm of the tax authorities. When a reputable Zeirishi firm represents a startup, the bank assumes that a baseline level of due diligence has already been performed. The accountant’s reputation is effectively on the line. Founders who attempt to open accounts solo often fail, while those accompanied by a senior partner from an established accounting firm find the process significantly smoother.

“The bank does not scrutinize your pitch deck; they scrutinize your footprint. They want to see a physical office with a lease in the company’s name, not a virtual office or a co-working space as proof that you have a physical stake in the Japanese soil.”

Another critical strategy involves the “Tiered Banking” approach. Attempting to start with a “Mega-bank” in Otemachi is a high-risk, low-reward opening move. Instead, founders should focus on three distinct tiers:

The Digital Challengers (Neobanks): Institutions like GMO Aozora Net Bank or Rakuten Bank have designed their onboarding processes for the modern era. They often accept online applications and are significantly more comfortable with foreign-led tech companies. They provide the initial operational beachhead.

The Regional and Shinkin Banks: Banks like Kiraboshi Bank or local Shinkin (credit unions) have a mandate to support regional business growth. They value the “face-to-face” relationship. A founder who takes the time to visit a local branch manager and explain their commitment to the local ward often finds a level of flexibility that is non-existent at the national majors.

The “Main Bank” Long Game: Once a startup has a year of domestic transactions, a physical office, and a handful of Japanese employees, the “Mega-banks” become much more receptive. The goal is to move up the hierarchy once you have a “history of existence” to present.

Here is the breakdown of the Global Expectation vs. the Japanese Banking Reality:

1. Physical Office Requirements

The Global Expectation: A virtual address or a co-working space membership is usually sufficient to get started.

The Japanese Reality: Banks almost always require a physical lease agreement. The space must typically have a dedicated entrance and a permanent signboard to prove the business actually exists at that location.

2. Representative Residency

The Global Expectation: Directors and representatives can often be based anywhere in the world, managing the account via digital portals.

The Japanese Reality: At least one representative director must typically hold a Japanese residency card (Zairyu). Without a local “face” for the company, most banks will reject the application immediately due to KYC (Know Your Customer) risks.

3. Paid-in Capital (資本金)

The Global Expectation: You can start with any nominal amount ($1 or $100) as long as you have enough to cover initial operations.

The Japanese Reality: While the law allows for 1-yen companies, banks view higher “paid-in capital” as a signal of stability and seriousness. Low capital is often a red flag that may lead to account denial.

4. Documentation & Signatures

The Global Expectation: Digital PDFs, DocuSign, and e-signatures are the standard for speed and efficiency.

The Japanese Reality: Prepare for a paper-heavy process. Banks require original certificates (like your Tokyobo) issued within the last 3 to 6 months, and most forms must be authorized using physical seals (Hanko/Inkan) rather than ink signatures.

The final piece of the strategy is “The Business Description.” In the US or Europe, a startup might describe its mission in broad, aspirational terms. In a Japanese bank application, the description must be granular and “traditional.” The bank needs to see a clear list of potential Japanese clients and a detailed explanation of the revenue model. They are looking for “predictability.” If your business model is too disruptive or involves complex “platform” mechanics that the branch manager does not understand, the application will be flagged as “high risk.” Frame your innovation as an “improvement of existing Japanese industrial processes” to gain the bank’s comfort.

The Bottom Line

A corporate bank account in Tokyo is the ultimate social credential, signifying that your firm has been vetted and accepted into the Japanese corporate family. Success requires moving beyond a transactional mindset and intentionally building a “network of trust” through local proxies like tax accountants and regional bank managers. By providing the bank with the physical and social proof they require, you transform your startup from a foreign outlier into a legitimate domestic player.

Over to You

Does your current expansion plan prioritize the establishment of a physical “trust footprint” in Japan, or are you still relying on the digital-first assumptions of your home market?